Guides

What happens to debt when you die?

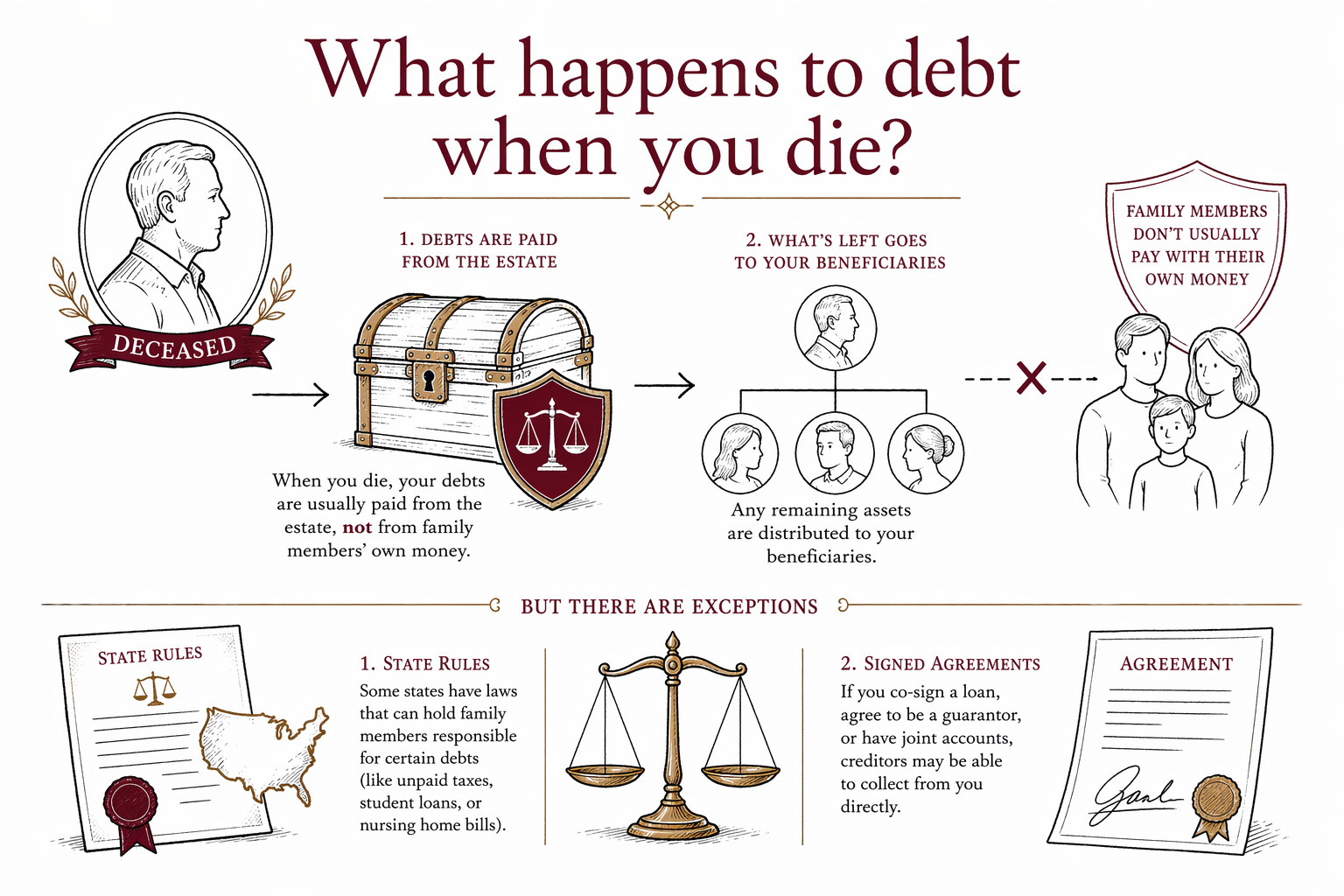

When someone dies, their debts do not simply disappear, but family members are usually not personally responsible unless they co-signed, guaranteed, or live in a community-property state where the rules can be different. The estate generally pays valid debts first, and state law controls the order and process.

Short answer: who pays the debt?

In many cases, debts are paid from the person’s estate after death. That means the money and property left behind may be used to pay certain bills before anything is passed to heirs.

If there is not enough money in the estate, some debts may go unpaid. Usually, family members do not have to pay a parent’s or spouse’s debt just because they are family.

There are important exceptions. If you signed the account, co-borrowed, guaranteed the loan, or held the debt jointly, you may still owe it. Rules also vary by state, especially for spouses and community property.

Which debts are usually handled first?

The exact order depends on state law, but the estate typically handles debts in a legal priority order. Common examples include funeral expenses, administration costs, taxes, secured debts, and then unsecured debts like credit cards.

A probate court or the person in charge of the estate may need to review claims and pay them from estate funds. If the estate is small or there is no probate, the process can be simpler, but the debt rules still matter.

Keep in mind that some debts are tied to a specific asset. For example, a car loan or mortgage is often secured by the car or house, so the lender may have rights against that property if payments stop.

What debts family members should watch for

Some debts are more likely to surprise families after a death:

- Joint credit cards or loans

- Co-signed student loans or personal loans

- Mortgages and car loans

- Medical bills

- Taxes owed by the person who died

- Home equity loans and other secured debts

Also watch for automatic payments and subscriptions tied to the person’s accounts. Those can keep running if no one closes or updates the accounts.

Common mistakes that make debt problems worse

A few planning mistakes can make things harder for family members:

- Dying without a will, which can lead to intestacy and a longer court process

- Out-of-date beneficiary designations on life insurance, retirement accounts, or payable-on-death accounts

- An unfunded trust, where the trust exists but key assets were never moved into it

- No named backup fiduciary, executor, or guardian

- Relying on DIY forms that do not meet your state’s rules

These problems do not create debt by themselves, but they can slow down estate administration and make it harder to pay valid bills on time.

What to do if a loved one died with debt

- Gather mail, account statements, and bills so you can see what exists.

- Stop and review automatic payments and subscriptions.

- Do not pay a debt from your own money until you know whether you are legally responsible.

- Find out whether the estate will go through probate in your state.

- Ask a licensed estate planning attorney in your state how local law handles creditor claims and spouse liability.

A lawyer can also help if the estate has a house, a trust, or debts that may be secured by property.

How WillArbor can help

WillArbor is a free matching service, not a law firm, and not your lawyer. We help you connect with a licensed estate planning attorney near you who can explain your state’s rules and help you plan ahead or handle a loved one’s estate.

You stay in control: you compare attorneys, choose who to hire, and confirm the flat fee in writing before any work starts. Most estate planning is quoted as a flat fee, not hourly, but the real number depends on the documents, the complexity, and the state. We do not draft documents or create an attorney-client relationship.

You only need to share contact information and planning intent, such as your state, what you want to plan, and your preferred language. If you are ready, start with get matched, or learn more in our guides and services.

When someone dies, debts are usually paid from the estate, not from family members’ own money, but state rules and signed agreements can change that.

Common questions

Do my children have to pay my debts when I die?

Usually, no. Children are generally not personally responsible unless they co-signed, jointly borrowed, or the law of your state creates a specific exception. The estate is usually the first place creditors look.

Can creditors take everything I leave behind?

Sometimes estate assets are used to pay valid debts, but the result depends on the type of debt, what property exists, and state law. Some assets may pass outside probate if they have named beneficiaries, but those rules also vary by state.

Do I need a lawyer to deal with a death and debt?

Often, yes, especially if there is a house, a trust, several debts, or confusion about who is responsible. A licensed estate planning attorney in your state can explain the local rules and help you avoid paying a debt you do not owe.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →