Guides

How to Avoid Probate

Avoiding probate usually means planning ahead so your important property passes to the right people without court delays. This guide explains the most common options families use, and where state rules can change.

The direct answer: the goal is fewer assets going through court

Probate is the court process that handles a person’s estate after they die. You can often reduce probate (or even avoid it for certain assets) by planning how property is owned and who is named to receive it.

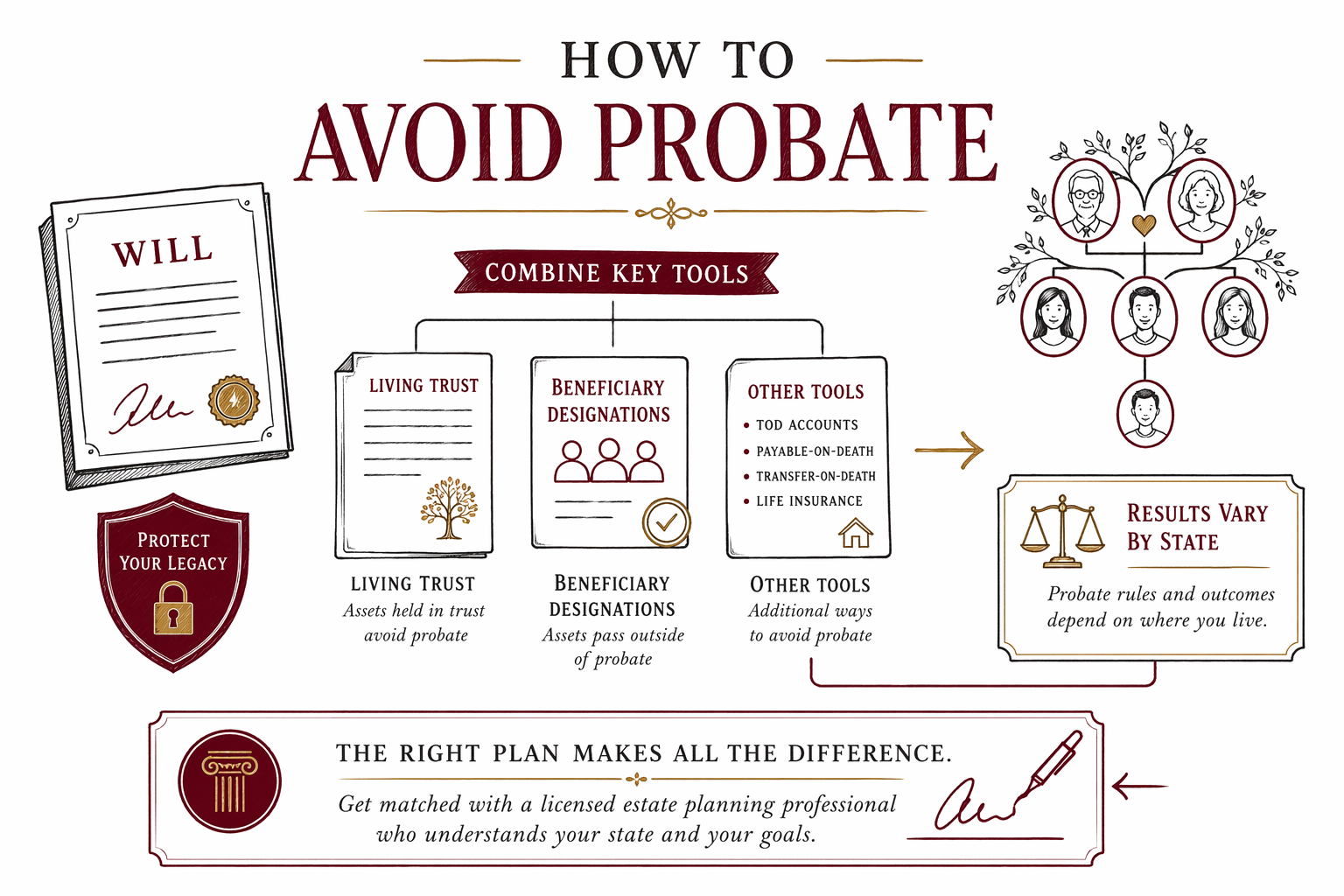

There is no single method that works everywhere, because probate rules and what counts as “probate property” vary by state. A licensed estate planning attorney in your state can confirm what will (and won’t) avoid probate for your situation.

Common ways families reduce probate

Many families use a mix of these tools. Think of them as “routes” that move property to the people you choose—without waiting for court approval.

1) Living trust (often reduces probate for assets titled to the trust)

A living trust can hold property during your life and provide instructions for what happens after death. If the right assets are properly “funded” into the trust, some or most of that property may bypass probate.

2) Beneficiary designations (often bypass probate)

Some accounts pass directly to named beneficiaries when someone dies (for example, certain retirement accounts, life insurance, and some payable-on-death or transfer-on-death arrangements).

3) Joint ownership or survivorship arrangements (may bypass probate, but not always)

Owning property with a right of survivorship can allow it to pass automatically to the surviving owner. However, joint ownership can have downsides, including effect on Medicaid eligibility in some states and unintended results for family members.

4) Payable-on-death / transfer-on-death (TOD/POD) on accounts

For some assets, you can name who receives them at death. These options can help avoid probate for that asset, depending on state law and how the asset is titled.

Practical steps to check your plan (and fix common problems)

Start with what you can control now. The most common issues aren’t unusual—many people simply haven’t reviewed their choices.

1. Make sure you have a current will (even if you’re also using a trust)

If you die without a will, your state’s “intestacy” rules decide who inherits and who may become a guardian for minor children.

2. Review beneficiary designations (they can override your will)

Beneficiary forms on accounts often control who gets those assets, regardless of what your will says.

3. Confirm property is titled the right way (especially for trusts)

A trust that isn’t properly funded may not reduce probate the way you expected. For example, if you meant for a home to be in the trust, it usually needs to be correctly titled.

4. Update plans after big life changes

Events like marriage, divorce, births, deaths in the family, moving to a new state, or changing immigration status can affect your plan.

5. Think about guardianship

If you have children, avoiding probate should not distract you from the most important part: naming a guardian for minors in a will (and ensuring the court can recognize it).

Pitfalls that increase the chance of probate

These are frequent reasons families end up dealing with court when they wanted to avoid it.

- Dying without a will (intestacy): your state decides key family matters.

- Out-of-date beneficiary designations: the form on file may not match your intentions.

- DIY forms that don’t match your state’s rules: paperwork that seems “right” may not do what you think.

- An unfunded trust: the trust exists, but assets weren’t transferred or titled correctly.

- Forgetting about debts and taxes paperwork (not advice, but planning helps): even if probate is reduced, certain notifications and filings may still be required.

- Not accounting for state-specific property rules: probate and non-probate property categories vary by state.

What to expect when you talk with an attorney

When you meet with a licensed estate planning attorney, you can ask questions focused on avoiding probate while still protecting your family.

Consider asking:

- Which assets are likely to go through probate in my state?

- Would a living trust help, or would beneficiary designations be enough?

- If I use a trust, what steps are needed to “fund” it?

- How do joint ownership choices work here, including any tradeoffs?

- What documents should also cover guardianship and medical decisions?

Cost note (honest, general): most estate planning work is quoted as a flat fee, not hourly. Common flat-fee ranges vary widely by state and complexity, but many families spend roughly $1,000–$3,500 for a basic plan (often a will and/or trust plus core documents), and more (often $3,000–$6,000+ and sometimes higher) if the plan is more complex or involves multiple trusts, more property types, or special circumstances. These ranges are not quotes—only an attorney can price your exact set of documents after reviewing your needs.

No guarantees: even a good plan can’t always eliminate probate in every scenario, because state law and how property is titled can affect outcomes.

Get matched with a licensed estate planning attorney (for free)

If you want help figuring out the best way to reduce probate for your family, WillArbor can connect you with a licensed estate planning attorney near you at no cost to you.

Use get matched and share only your contact info, your state, and what you want to plan (for example: “reduce probate,” “set guardianship,” or “set up powers of attorney”). We don’t ask for asset values, account numbers, document contents, or Social Security numbers.

Then, compare attorneys and confirm the flat fee in writing before any work starts. For general education, explore guides and services while you prepare for your conversation. Estate planning rules vary by state—so always confirm details with a licensed attorney in your state.

To reduce probate, families usually combine a will with tools like living trusts and beneficiary designations, but the exact results depend on your state—so get matched with a licensed estate planning attorney in your area and confirm a flat fee in writing.

Common questions

Does a will avoid probate?

A will usually does not fully avoid probate. In many cases, probate is still needed to prove the will and handle the estate’s probate assets, although the will can guide who inherits and how debts and expenses are handled. Other tools—like a living trust or beneficiary designations—may reduce probate for certain assets.

Can I avoid probate completely?

Sometimes probate can be reduced significantly, and some assets may pass outside probate. But complete avoidance is not guaranteed and depends on state law and how property is titled or designated. A licensed estate planning attorney can explain what “avoid probate” means in your state for your specific situation.

What’s the biggest mistake families make when trying to avoid probate?

A common mistake is having a trust (or other documents) but not titling or funding assets the way the plan requires, plus forgetting to keep beneficiary designations up to date. Another frequent issue is relying on DIY forms that don’t match your state’s rules.

Do beneficiary designations override a will?

Often they do. Many account types and some insurance or transfer-on-death arrangements pass to named beneficiaries based on the beneficiary form, not the will. That’s why reviewing beneficiary designations after life changes is important.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open → What Estate Planning Really CostsFlat fees vs hourly billing, typical ranges by document, and how to avoid overpaying.

Open →