Guides

What is a spendthrift trust?

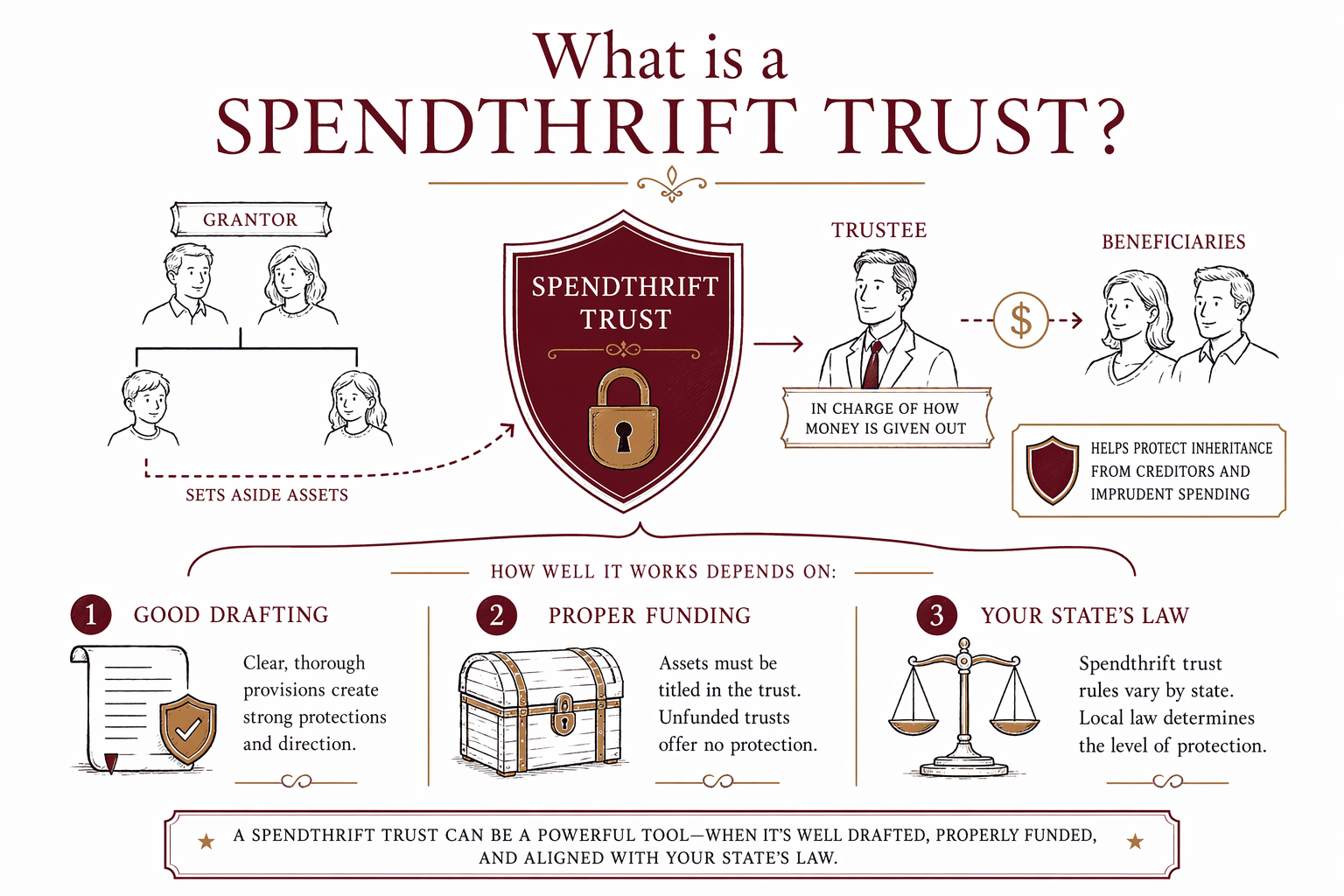

A spendthrift trust is a trust designed to help protect money or property for a beneficiary who may spend too quickly, have creditors, or need help managing an inheritance. It can be useful in some families, but the rules and limits vary by state.

The short answer

A spendthrift trust is a type of trust that limits a beneficiary's direct control over the assets in the trust. Instead of receiving the whole inheritance at once, the beneficiary receives money or support under rules written into the trust and managed by a trustee.

The goal is usually protection. A spendthrift trust may help protect trust assets from a beneficiary's own impulsive spending, and in some situations it may also make it harder for certain creditors to reach what is still inside the trust. But it is not a magic shield, and the exact protection depends on state law, the trust language, and the facts of the situation.

This is general educational information only, not legal, tax, or financial advice. Trust law varies by state and changes over time, so it is smart to speak with a licensed estate planning attorney in your state before setting one up.

How it works in everyday terms

Think of it this way: instead of leaving a child or other loved one a large lump sum, you place the inheritance into a trust. You then name a trustee — the person or institution who manages the trust — and set rules for when and how the beneficiary receives money.

For example, the trust might allow the trustee to pay for health, education, housing, or other support. Or it might direct small monthly distributions instead of one big payout at age 18. The beneficiary may benefit from the assets, but may not be allowed to sell, assign, or demand the full amount whenever they want.

That structure is what gives a spendthrift trust its name. The trust is meant to reduce the risk that the inheritance will be spent too fast or lost soon after it is received.

Why families use a spendthrift trust

Families often consider a spendthrift trust when they want to leave help, but also want guardrails. This can come up if a beneficiary is young, has trouble managing money, is in a risky marriage, has a disability, has addiction concerns, or is simply vulnerable to pressure from others.

A spendthrift trust can also help when a parent or grandparent wants to avoid giving a large inheritance all at once. Instead, the trustee can follow the instructions in the trust over time.

In some cases, families also hope for creditor protection. That may exist to some extent while assets remain in the trust, but there are important exceptions under many state laws. Child support, spousal support, taxes, and certain other claims may be treated differently. Once money is distributed to the beneficiary, protection may be lost.

If your main goal is broader family planning — like avoiding probate, choosing who inherits, naming guardians, and coordinating powers of attorney — it may help to read more in our guides or explore common services.

What a spendthrift trust can and cannot do

A spendthrift trust may help control timing and use of an inheritance. It may help reduce waste, delay access until a safer age, and give a responsible trustee authority to manage assets for the beneficiary's benefit.

But it does not solve every problem. It does not guarantee protection from all creditors. It does not replace good trustee choice. It does not fix poor drafting. And if the trust is not properly created or funded, it may not work as intended.

A common misunderstanding is that any trust automatically protects assets. That is not true. Some trusts are revocable and remain closely tied to the person who created them during life. Some protections only apply after death, or only if the trust is drafted in a certain way. State law matters a great deal here.

Common pitfalls to avoid

One pitfall is using a DIY form that does not fit your state. Trusts are not one-size-fits-all, and wording matters. A document that sounds right in plain English may still fail to do what your family wanted.

Another common problem is an unfunded trust. Even a well-written trust may not help if assets are never transferred into it or beneficiary designations are not coordinated. Families are often surprised to learn that a trust only controls the assets that actually pass into the trust.

There are also bigger estate-planning mistakes that connect to this topic:

- Dying without a will, which means state intestacy rules decide who inherits

- No named guardian for minor children

- Out-of-date beneficiary designations on retirement accounts or life insurance

- Choosing the wrong trustee, or not naming a backup trustee

- Assuming a trust avoids every probate or creditor issue automatically

Because rules vary by state, a licensed estate planning attorney can help you see whether a spendthrift trust fits your real goals, or whether a simpler will or living trust would be enough.

What it may cost and how to get help

A spendthrift trust is usually part of a broader estate plan prepared for a flat fee, not hourly, though practices differ. In many states, a simple will-based plan may be a few hundred to around $1,500, while a revocable living trust estate plan is often roughly $1,500 to $5,000 or more. If you want more customized trust terms, planning for a vulnerable beneficiary, tax issues, blended-family concerns, or multiple properties, the flat fee may be higher. These are general ranges, not quotes.

The real price depends on the documents you need, the complexity of your family and assets, and your state. Before any work starts, ask the attorney to confirm the flat fee in writing, explain what documents are included, and tell you whether funding help is included.

WillArbor is a free matching service, not a law firm, not a lawyer, and does not draft documents or create an attorney-client relationship. We can help you get matched, free, with a licensed estate planning attorney near you or one serving your state. You stay in control: compare attorneys, ask questions, confirm the bar license, and decide who to hire.

If you want help finding someone, you can get matched. We only collect basic contact and planning intent information — such as your name, phone, optional email, state, what you want to plan, and preferred language — not account numbers, asset values, or sensitive estate details.

A spendthrift trust can help protect an inheritance by putting a trustee in charge of how money is given out, but whether it works well depends on good drafting, proper funding, and your state's law.

Common questions

Is a spendthrift trust only for people who are bad with money?

No. Families also use them for young beneficiaries, blended families, beneficiaries facing pressure from others, or anyone who may need long-term structure instead of a lump sum.

Does a spendthrift trust protect assets from all creditors?

Usually not. Some protection may exist while assets remain in the trust, but exceptions are common and the rules vary by state. Once funds are distributed, they are often much easier for creditors to reach.

Can I make a spendthrift trust in my will?

Sometimes, yes. A trust can be created under a will or as a separate trust document, depending on the plan. What works best depends on your goals, the beneficiary, and your state's rules.

Who should be the trustee?

Choose someone responsible, organized, and able to follow the trust terms fairly. That might be a trusted relative, a friend, or a professional trustee, depending on the situation.

Do I need both a will and a trust?

Maybe. Many estate plans include both, because they do different jobs. An estate planning attorney can explain whether you need a will alone, a living trust plan, or a trust for a specific beneficiary.

How do I find the right attorney?

Look for a licensed estate planning attorney in your state, ask about experience with trusts for beneficiaries, and confirm the flat fee in writing before work begins. WillArbor can help you get matched for free, but we are not a law firm and not your lawyer.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →