Your situation

Estate Planning for Single Adults

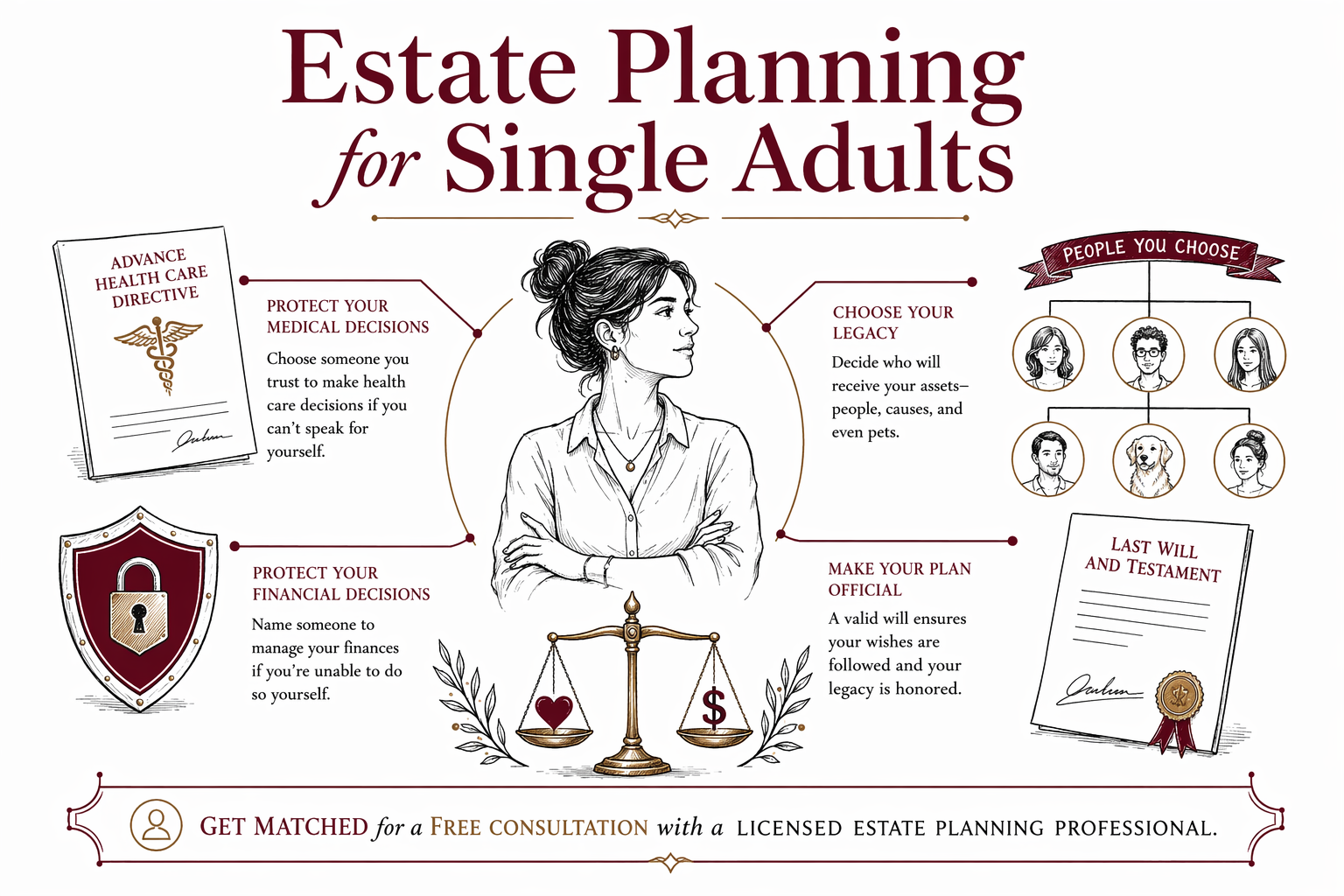

If you’re a single adult, estate planning can still protect you and the people you care about—especially through a power of attorney and an advance directive. It’s also how you decide who gets your assets and who handles your affairs if you can’t.

Why estate planning matters when you’re single

A lot of people think estate planning is only for married couples or parents. But being single doesn’t remove the need to plan—life events can happen to anyone.

Your documents can help make sure your wishes are followed if you become unable to make decisions, and your property is handled the way you choose after death. Without a clear plan, families often spend more time and energy sorting things out.

Estate planning rules and probate procedures vary by state, so this page is general education. For your exact options, it’s best to talk with a licensed estate planning attorney in your state.

Core documents to consider (and what they do)

Many single adults start with a small set of documents. The right combination depends on your state and your situation, but these are common building blocks.

1) Will: A will usually tells the court who should receive your assets after you pass away, and it can name a personal representative to manage the estate.

2) Advance Directive (Living Will) + Health Care Power of Attorney: These cover medical decisions if you can’t speak for yourself. The “advance directive” typically addresses your wishes about end-of-life care, while a health care power of attorney names someone to make medical decisions.

3) Financial Power of Attorney: A power of attorney can allow someone you trust to handle financial matters if you become unable to manage them. In some cases, you’ll want it to apply immediately, and in others you’ll want it to activate only if you’re determined unable—an attorney can explain the differences in your state.

If you own a home, have concerns about probate, or want more control over how things pass, you may also discuss whether a living trust or other plan makes sense. An attorney can help you compare options based on your state’s rules.

Who you should name (even if you don’t have a spouse)

A common fear is, “Who will speak for me?” Estate planning is where you choose those people on purpose.

For healthcare decisions, think beyond who “might be available.” Choose someone who is willing to talk with doctors, ask questions, and follow your values and medical preferences.

For financial decisions, choose someone who handles bills, paperwork, and deadlines responsibly. It also helps to name alternates—someone else who can step in if your first choice can’t.

For your will, you should clearly identify beneficiaries and (where applicable) alternate beneficiaries so that your wishes aren’t slowed down by ambiguity.

Common pitfalls for single adults (easy to miss)

Here are issues that come up often when people haven’t planned—or planned in a way that doesn’t fit their state.

- Dying without a will (often called “intestacy”): state default rules decide who receives your assets, which may not match what you wanted.

- DIY forms that don’t match your state: requirements can be specific, and incorrect wording can cause delays.

- Out-of-date beneficiary designations: even with a will, some accounts (like certain retirement plans or insurance) may pass to named beneficiaries based on the forms on file.

- A trust that isn’t “funded”: if you use a trust, assets often must be titled or assigned appropriately for the trust to do what you expect.

- Not naming a guardian (only relevant if you have minor children): if you have children, your plan should clearly name guardians and backups.

These are general examples. A licensed estate planning attorney can help you avoid problems that are specific to your state.

What estate planning can cost (typical flat-fee ranges)

Most estate planning work is quoted as a flat fee rather than hourly. A fair flat fee depends on which documents you need, the complexity of your situation, and your state.

As general guidance, many single adults might see flat-fee ranges such as:

- Will + basic advance directive/health care power of attorney: often in the low to mid hundreds, up to around the low thousands in some states

- Will plus a financial power of attorney: often adds to the range above

- More involved plans (for example, adding a living trust, or coordinating more complicated beneficiary goals): often move into higher flat-fee ranges

These ranges are not quotes. Your real price depends on what you’re asking to include and how the documents fit state requirements. When you talk with an attorney, ask what’s included in the flat fee and confirm the fee in writing before any work starts.

How to find a licensed estate planning attorney (and how WillArbor helps)

WillArbor is a FREE matching service. We connect you with licensed estate planning attorneys near you, based on what you want to plan and your preferred language. We are not a law firm and we don’t draft documents, and we don’t provide legal advice.

To get started, visit get matched. You’ll share contact details and your planning intent (for example: will, health care power of attorney, financial power of attorney). We do not ask for asset values, account numbers, Social Security numbers, or sensitive estate details.

Before you hire anyone, confirm they are licensed to practice in your state and ask questions like:

1. Which documents do you recommend for a single adult in this state?

2. What’s included in your flat fee?

3. How do you handle updates later if my situation changes?

Then you stay in control: compare attorneys, ask for explanations in plain language, and choose who to hire.

Even if you’re single, planning ahead helps protect your medical and financial decisions and makes sure your assets go to the people you choose—so get matched for a free consultation with a licensed estate planning attorney.

Common questions

I don’t have a spouse or kids. Do I really need a will?

Yes, a will can still be important because it tells the court who you want to receive your assets. If you don’t have one, your state’s default “intestacy” rules decide, which may not match your wishes.

What’s the difference between a living will and a health care power of attorney?

A living will generally describes your wishes about certain medical situations. A health care power of attorney names a person to make medical decisions for you if you can’t—especially when doctors need guidance and there isn’t a clear instruction.

Should I set up a financial power of attorney even if I’m healthy?

Many people do. A financial power of attorney can help if you’re temporarily or permanently unable to manage bills, banking, or paperwork. The exact “when it starts” language varies by state, so it’s worth discussing with a licensed attorney.

If I have beneficiaries on some accounts, does that replace estate planning?

Beneficiary designations can control how some accounts pass, but they usually don’t cover everything. A will and your healthcare/financial documents may still be needed to address assets, decision-making, and situations your beneficiary forms don’t cover.

How do I avoid probate?

Avoiding or reducing probate depends on your state and your goals. Some people use certain strategies (like trusts), but whether that makes sense for you depends on your overall plan and state rules—an attorney can help you compare options.

How much does estate planning cost for a single adult?

Cost varies by state and by which documents you need. Many plans are quoted as flat fees, often in the low hundreds to low thousands for common document sets, but this is not a quote. Ask each attorney what’s included and confirm the fee in writing.

Related help

Guardians, a will, and a simple plan so your children are cared for if something happens to you.

Open → Estate Planning for HomeownersHow to keep your home out of probate and pass it to the people you choose.

Open → Estate Planning for Blended FamiliesPlans that protect a current spouse and children from a previous relationship — fairly and clearly.

Open →