Guides

What is a payable on death account?

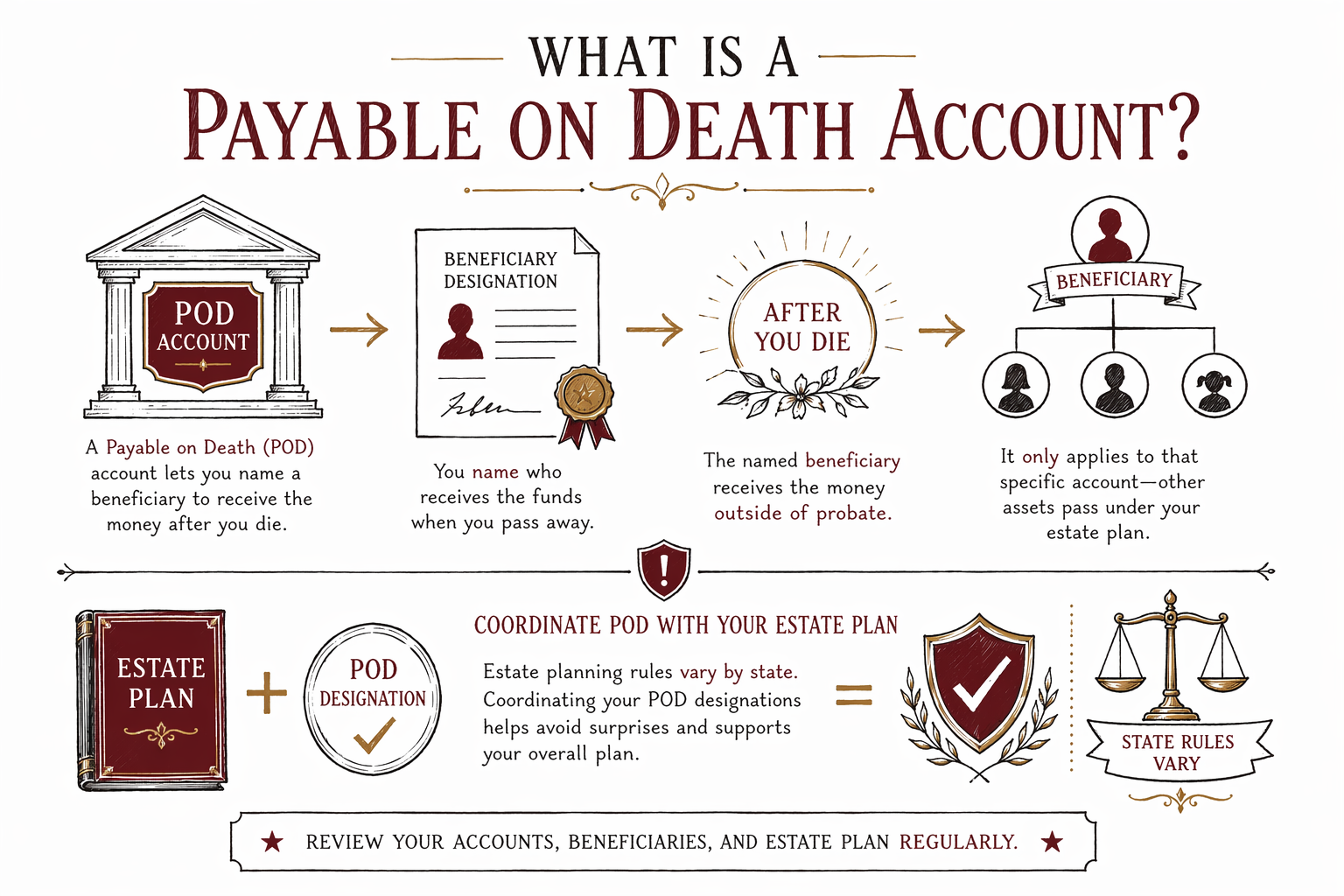

A payable on death (POD) account lets the owner name who should receive the money after they die, without going through probate. The best next step is to understand how POD works in your state and how it fits with your will or trust.

Payable on death (POD), in plain terms

A payable on death (POD) account is a way to pass money after your death to someone you choose, usually by listing a beneficiary when you open the account.

In many cases, the money goes to the named beneficiary directly after the death certificate is provided, which can reduce or avoid probate. But what “counts” as POD, and exactly how it is handled, depends on state law and the account agreement.

POD is not the same as a will. Your will may still matter for other assets, for naming guardians, and for covering gaps—especially if someone you named can’t receive the account or is not the right person under your situation.

How a POD account is handled when someone dies

Usually, the account holder names a POD beneficiary. After the account holder dies, the beneficiary typically provides proof of death and identity to the bank or financial institution to receive the funds.

Because the transfer is handled through the institution, POD can be simpler than probate for that specific account. However, you still want a complete estate plan, because POD does not automatically solve every issue—such as guardianship for minor children or debts and taxes that may come up.

Rules vary by state, and account contracts can differ. A licensed estate planning attorney in your state can help you understand how POD interacts with your will or trust.

POD vs. “will” vs. “trust” (quick difference that matters)

A will is a written legal document that explains what happens to your assets after you die, and it can name guardians for children. A trust is a legal arrangement where a trustee manages assets for beneficiaries under instructions you set up.

A POD account is neither a will nor a trust—it’s an account feature. The beneficiary designation generally controls who receives that specific account.

This is why it’s important to keep beneficiary information current and make sure it matches your overall plan. If a POD beneficiary is outdated, a will might conflict with the account, or an intended recipient might not receive what you expected.

Common pitfalls families run into with POD accounts

Many POD problems come from simple mismatches or outdated info. Here are a few common pitfalls to watch for:

- Dying without a will (called intestacy): your will-related goals—like guardianship—may not be handled the way you want, even if some accounts use POD.

- Out-of-date beneficiary designations: people change their minds, then forget to update POD after a divorce, remarriage, or family changes.

- Assuming POD “overrides everything”: POD may control that account, but other assets (and decisions like guardianship) may still depend on your will or trust.

- Relying on DIY forms that don’t fit your state: estate planning rules vary by state, and the wrong approach can cause delays or confusion.

- Using an unfunded trust mindset: a trust only helps if the right assets are properly moved into it, while POD beneficiary designations are handled through the account provider.

How to make POD part of a solid estate plan

To use POD wisely, treat it as one “piece” of your plan—not the entire plan.

- Step: Confirm which of your accounts are set up as payable on death (POD) and who the current beneficiary is.

- Step: Check whether your will and other documents reflect your real intentions, especially if your family situation has changed.

- Step: If you have minor children or someone who needs care, make sure you’ve covered guardianship in a will or other appropriate document.

- Step: If a trust is part of your plan, ask how POD interacts with it and whether any accounts should be moved or re-titled.

Rules vary by state. A licensed estate planning attorney can review your documents and account beneficiary designations to help you avoid unintended results.

Costs and what to expect when you talk to an attorney

Talking to a licensed estate planning attorney can help you understand how POD accounts work in your state and how to coordinate them with your will or trust. Most estate planning is quoted as a flat fee, not hourly, but the real number depends on what you need.

Typical flat-fee ranges (for many families) often fall around:

- Will-based plans: roughly $1,000–$3,000

- Trust-based plans (more complex): roughly $2,000–$6,000+

- Add-ons (like powers of attorney or health directives): sometimes increase the total depending on what’s included

These are broad ranges, not quotes. Costs can be higher if the situation is more complex (for example, multiple properties, blended families, special needs planning, or coordinating trust funding). Confirm the flat fee in writing before any work begins, and verify the attorney’s bar license in your state.

WillArbor is a FREE matching service that helps you connect with a licensed estate planning attorney near you. Use our get matched option to share your state and preferred language—then you can talk with an attorney directly. WillArbor is not a law firm and does not draft documents or provide legal advice.

A payable on death (POD) account is a way to name who receives certain money after you die, but it only covers that account—estate planning rules vary by state, so it’s smart to coordinate POD with a will or trust by talking with a licensed attorney.

Common questions

Does a POD beneficiary automatically get the money right after I die?

Often, yes—once the beneficiary provides a death certificate and the required paperwork to the account holder (like a bank or brokerage). Exact steps and timing can vary by state and by the account’s rules.

If I have a POD account, do I still need a will?

Usually, yes. POD can help transfer that specific account, but a will is often needed for other assets and—importantly—for naming guardians for minor children. If you’re unsure, talk with a licensed estate planning attorney in your state.

What happens to a POD account if I didn’t name a beneficiary?

If a POD beneficiary is missing or not valid, the account may be handled differently than you expect, which could lead to delays or probate involvement. Because the outcome varies by state and the account agreement, it’s best to review your options with an attorney.

Can my POD beneficiary be changed later?

In many cases, yes—you can update beneficiaries while you’re alive, following the account provider’s process. Make sure you update other parts of your plan too so your will/trust and beneficiary designations align.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →