Guides

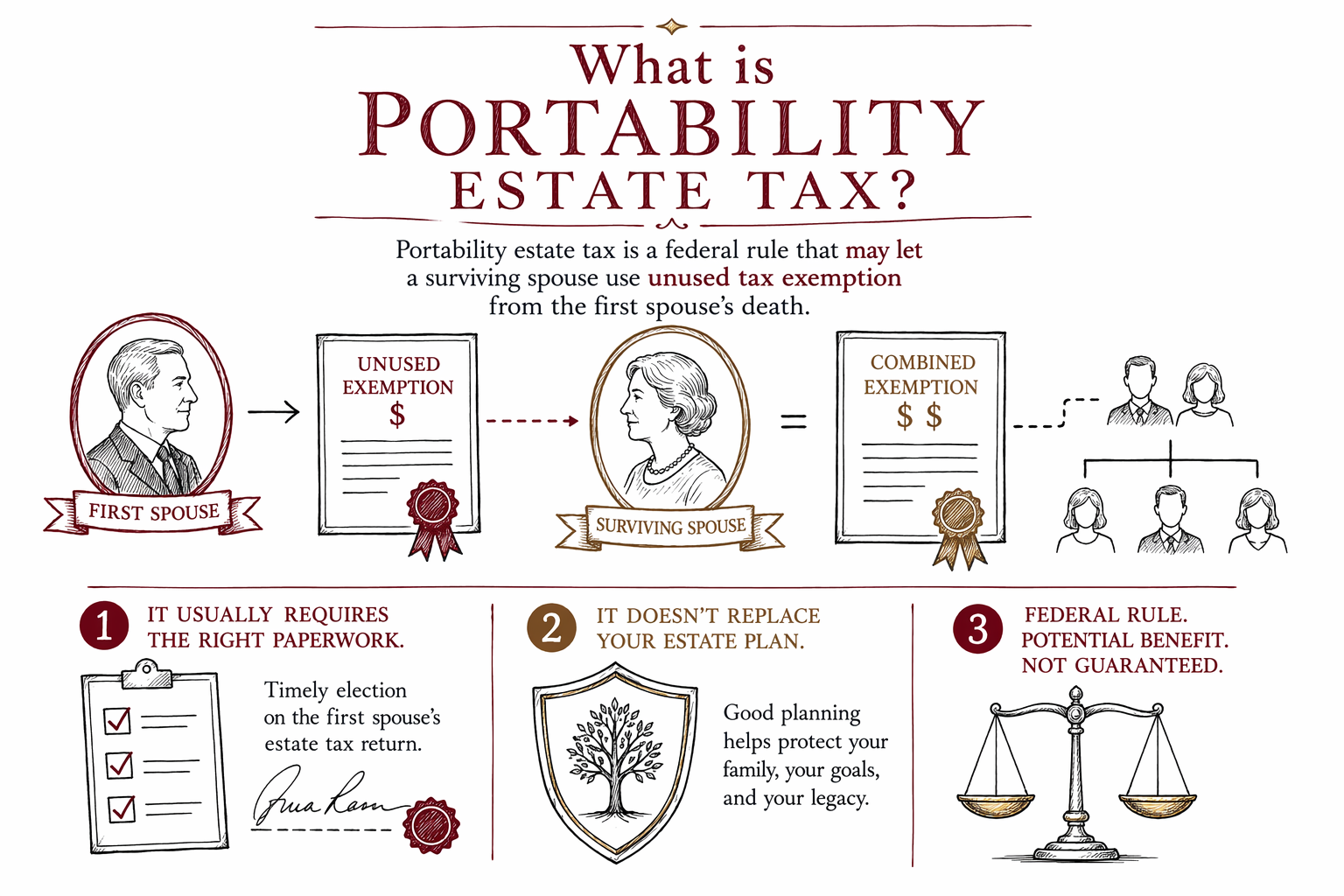

What is portability estate tax?

Portability estate tax is a U.S. tax rule that can allow a married couple to “carry over” part of an unused federal estate tax exemption from a deceased spouse to the surviving spouse. This guide explains what it is and what families should ask a licensed estate planning attorney.

Quick answer: what portability estate tax means

Portability estate tax is a federal rule for married couples. When the first spouse dies, the surviving spouse may be able to use the first spouse’s unused federal estate tax exemption (the “exemption amount”)—but only if the necessary paperwork is filed on time.

This rule is often discussed during estate planning because it can affect how much estate tax (if any) might be owed and how you structure documents. It does not automatically apply in every situation, and it doesn’t replace the basics of having a will or a trust.

Rules and forms can be complex, and the best plan depends on your state, your family situation, and your goals. Estate-planning attorneys can explain how portability may (or may not) fit for you.

How portability works, in plain steps

In simple terms, portability is about unused exemption from the first death. If the executor files an election with the federal tax return for the deceased spouse, the unused exemption can be carried over to the surviving spouse.

Because the details depend on timing and paperwork, portability is not something to assume will happen later. It’s usually handled right after the first spouse’s death.

For families, the practical takeaway is: plan ahead so the right election can be made if it’s appropriate.

- It generally requires an election/filed paperwork after the first spouse dies.

- It’s federal (U.S.)—but state estate and inheritance rules can be different.

What portability does—and doesn’t—do for families

Portability can help preserve the surviving spouse’s federal estate tax exemption, which may reduce or eliminate federal estate tax exposure in some cases.

But portability does not replace estate planning documents. A will, trust (if used), and decisions like guardianship for children and who inherits still matter. Also, portability usually affects federal estate tax exemption—not other important issues like probate, beneficiary choices, or how quickly assets can be distributed.

Many families still use trusts, beneficiary designations, and carefully chosen ownership to meet goals beyond federal estate tax.

State matters: rules vary by state

Even though portability is a federal concept, your overall plan can still be shaped by your state. Probate rules, how estates are administered, and whether your state has its own estate or inheritance taxes can vary a lot.

This is why two families with the same “federal portability” question may end up with different recommendations depending on where they live. Ask an attorney in your state to review your situation in the context of both federal and state rules.

If you want a starting point, you can browse WillArbor guides or learn about estate planning services and then get matched to a licensed attorney.

Common pitfalls families run into

Portability can be missed or made harder if the right forms aren’t filed after the first death. Another common issue is assuming “we’ll handle it later,” when in reality elections and paperwork deadlines can be strict.

A different pitfall is focusing only on tax ideas and forgetting the human and legal basics: who should get the assets, who should make decisions if someone becomes unable to act, and—if there are children—who should be the guardian.

You can also run into trouble with DIY forms that don’t fit your state, or with outdated beneficiary designations that conflict with your overall plan.

- Dying without a will (intestacy) or with documents that don’t match your intentions.

- Assuming portability is automatic—when it may require a federal election after the first death.

- Out-of-date beneficiary designations or account titling that override your plan.

- DIY forms that may not work in your state.

What to ask a licensed estate planning attorney

Because portability depends on details and timing, it helps to come prepared with questions—not asset values or account numbers. A good starting conversation can be calm and practical.

Consider asking:

1. Whether portability is relevant for your family and goals.

2. What documents and steps would be needed after the first spouse’s death (and who would do them).

3. How your state’s probate and tax rules may interact with federal portability.

4. Whether a trust or other plan design is recommended instead of relying on portability alone.

You should also confirm the attorney’s bar license and ask how they quote fees. Most estate planning work is quoted as a flat fee (not hourly). Cost depends on the documents, complexity, and your state—so any range you see is informational, not a promise.

- Most families do best with a plan that covers taxes and the everyday legal protections (will/trust, powers of attorney, directives).

- Fees vary, so confirm the flat fee in writing before any work starts.

Cost expectations (plain ranges) for estate planning discussions

If you’re trying to understand portability as part of estate planning, the cost is usually tied to what documents you need—not just the tax concept. Many attorneys quote estate planning as a flat fee.

In general, families may see flat-fee ranges like:

- Basic plan (often a will plus key decision documents): roughly $1,500–$4,000

- More involved planning (often adding a living trust and/or additional structures): roughly $3,000–$8,000+

These are not quotes and not guaranteed prices. The true cost depends on your state, how complex your goals are, and what documents are recommended. Ask the attorney to explain what is included and confirm the flat fee in writing before work begins.

If cost is a concern, you can still start by getting matched. WillArbor is free for families and can connect you with a licensed attorney to discuss your options.

Portability estate tax is a federal rule that may let a surviving spouse use unused tax exemption from the first spouse’s death, but it usually requires the right paperwork and it doesn’t replace your state-based estate planning documents.

Common questions

Is portability estate tax the same as an estate tax exemption?

Portability is a rule that can let a surviving spouse use a deceased spouse’s unused federal estate tax exemption, if the required federal election paperwork is filed after the first death. It’s related to the exemption, but portability is the mechanism for carrying over unused amounts.

Does portability automatically apply when my spouse dies?

Often, it does not happen automatically. The executor typically must file the right election paperwork on time after the first spouse’s death for portability to be available.

Will portability replace my will or trust?

No. Portability (when it applies) is about federal estate tax exemption. It does not replace core planning documents like a will, trust (if used), powers of attorney, or advance directives.

If portability is federal, why do I need to talk to an attorney in my state?

Because estate planning rules and probate processes vary by state, and some states have their own tax rules. A licensed estate planning attorney in your state can explain how portability fits with local requirements.

What should I bring to my first meeting about portability?

Bring your goals and basic family information—such as whether you’re married, whether children are involved, and what concerns you most (protecting a spouse, avoiding probate, guardianship). Avoid sharing sensitive details like account numbers or SSNs unless your attorney asks through a secure process.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →