Guides

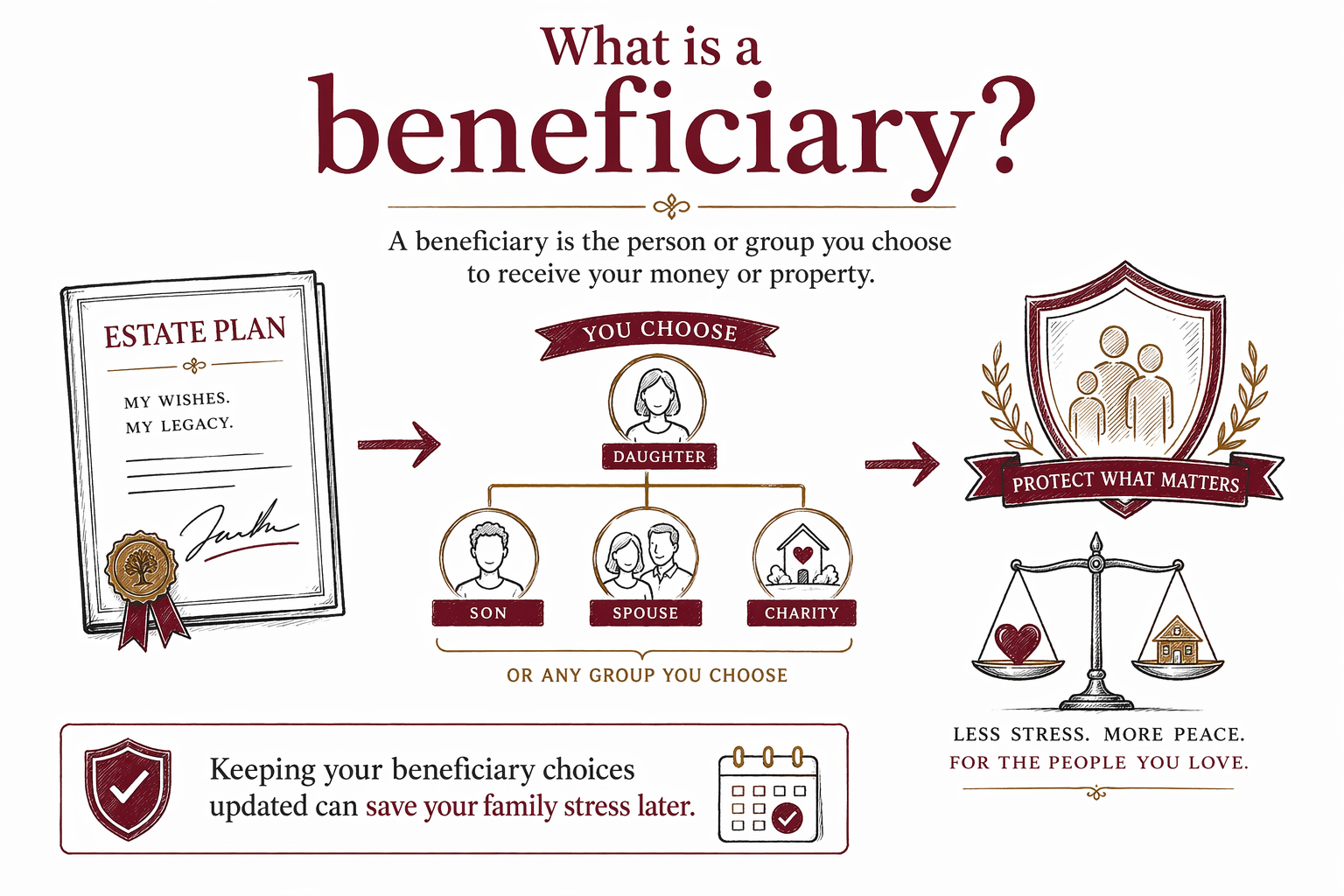

What is a beneficiary?

A beneficiary is the person or organization you choose to receive money, property, or other benefits after your death — and sometimes during your life through certain accounts or trusts.

What “beneficiary” means in plain English

A beneficiary is who you want to receive something you own or control. That could be money from a life insurance policy, funds in a retirement account, property named in a will, or assets held in a trust.

The word sounds technical, but the idea is simple: it answers the question, “Who gets what?” If you are planning for your family, naming the right beneficiaries is one of the most important parts of estate planning.

There is one important detail many families miss: a beneficiary named on an account is not always the same as a person named in a will. In many cases, the beneficiary form on the account controls first. That is why out-of-date beneficiary designations are a common and costly problem.

Where beneficiaries are used

You may name beneficiaries in several places. Common examples include life insurance, retirement accounts such as 401(k)s and IRAs, payable-on-death bank accounts, transfer-on-death accounts, wills, and living trusts.

A will can name who should inherit your property after death. A trust can also name beneficiaries and set rules for when and how they receive assets. For example, a trust may hold money for a child until the child reaches a certain age.

Some accounts pass directly to the named beneficiary without going through probate. That can be helpful, but it also means your overall plan can become inconsistent if your account forms do not match your will or trust. This is one reason many families ask a licensed estate planning attorney to review the full picture.

Primary, contingent, and minor beneficiaries

A primary beneficiary is first in line to receive the asset. A contingent beneficiary is the backup person or organization who receives it if the primary beneficiary has already died or cannot receive it.

Naming both primary and contingent beneficiaries can prevent confusion later. If you only name one person and that person dies before you, the asset may end up going through probate or being distributed under plan rules you did not expect.

If you want to leave money to a minor child, extra care is needed. In many cases, a minor cannot directly control inherited money or property. A will or trust may need to name a guardian, custodian, or trustee to manage it. Rules vary by state, so this is a good place to get state-specific legal help.

How beneficiaries fit with wills, trusts, and probate

Beneficiaries are part of a larger estate plan. A will can name who inherits property and who will care for minor children. A living trust can hold assets during your life and pass them to beneficiaries after death, often with more privacy and control.

Probate is the court-supervised process for settling certain property after a death. Property with a valid beneficiary designation may pass outside probate, while property with no beneficiary or no other transfer method may need to go through probate. An unfunded trust is another common pitfall: if assets were never moved into the trust, they may still end up in probate.

Dying without a will is called intestacy. When that happens, state law decides who inherits, which may not match what you wanted. Because probate and inheritance rules vary by state, general information online can only go so far.

Common mistakes families make

The most common problem is thinking a will automatically updates every account. Usually it does not. If your life changes — marriage, divorce, a new baby, a death in the family, or moving to a new state — your beneficiary forms and estate documents should be reviewed.

Another mistake is using DIY forms that do not meet your state's rules or do not work well together. Families also forget to name a backup beneficiary, forget to name a guardian for children, or create a trust but never transfer assets into it.

Watch for these common pitfalls:

- Dying without a will (intestacy)

- Out-of-date beneficiary designations

- DIY forms that fail in your state

- An unfunded trust

- No named guardian for minor children

When to talk with an estate planning attorney

You may want legal help if you have children, a blended family, a child with special needs, property in more than one state, a small business, or any concern that family members may disagree later. A licensed estate planning attorney can help make sure your beneficiary designations, will, trust, powers of attorney, and advance directives work together.

In many states, basic estate planning is priced as a flat fee rather than hourly. Very general ranges — not quotes — are often around $300 to $800 for a simple will package, $1,000 to $3,500 or more for a more complete plan, and roughly $2,000 to $6,000 or more for a trust-based plan, depending on the documents, the complexity, and the state. Ask for the flat fee in writing before work starts.

WillArbor is a free matching service, not a law firm and not your lawyer. We do not draft documents or create an attorney-client relationship. We can help you get matched with a licensed estate planning attorney near you, and your family stays in control — you compare attorneys, choose who to hire, and confirm the flat fee in writing.

To get started, you can explore more guides or services. If you want a referral, we only collect contact and planning intent: your name, phone, optional email, state, what you want to plan, and preferred language — never asset values, account numbers, or other sensitive estate details.

A beneficiary is the person or group you choose to receive your money or property, and keeping those choices updated can save your family stress later.

Common questions

Is a beneficiary the same as an heir?

Not always. A beneficiary is someone you name to receive an asset or benefit, while an heir is someone who may inherit under state law if there is no valid will. Rules vary by state.

Does my will control who gets my life insurance or retirement account?

Often, no. Many life insurance and retirement accounts follow the beneficiary form on file first, not the will. That is why it is important to keep those designations current.

Can I name my child as a beneficiary?

You can often name a child, but a minor usually cannot directly manage inherited assets. A trust, custodian, or other arrangement may be needed, and the rules vary by state.

What happens if I do not name a beneficiary?

It depends on the account, document, and state law. The asset may go to a default person under the contract, to your estate, or through probate, which can cause delay and extra cost.

How often should I review my beneficiaries?

A good rule is to review them after major life changes such as marriage, divorce, birth, death, or moving to a new state. Even without big changes, many families review every few years.

Can WillArbor tell me who I should name?

No. WillArbor is a free matching service, not a law firm and not your lawyer, so we only provide general educational information. For advice about your situation, speak with a licensed estate planning attorney in your state and confirm the attorney's bar license.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →