Guides

How to fund a living trust?

A living trust is “funded” by moving the right assets into it so your trust can hold and use them. The exact steps depend on state rules and your situation, so review this guide and confirm details with a licensed estate planning attorney.

The direct answer: what “funding” a living trust means

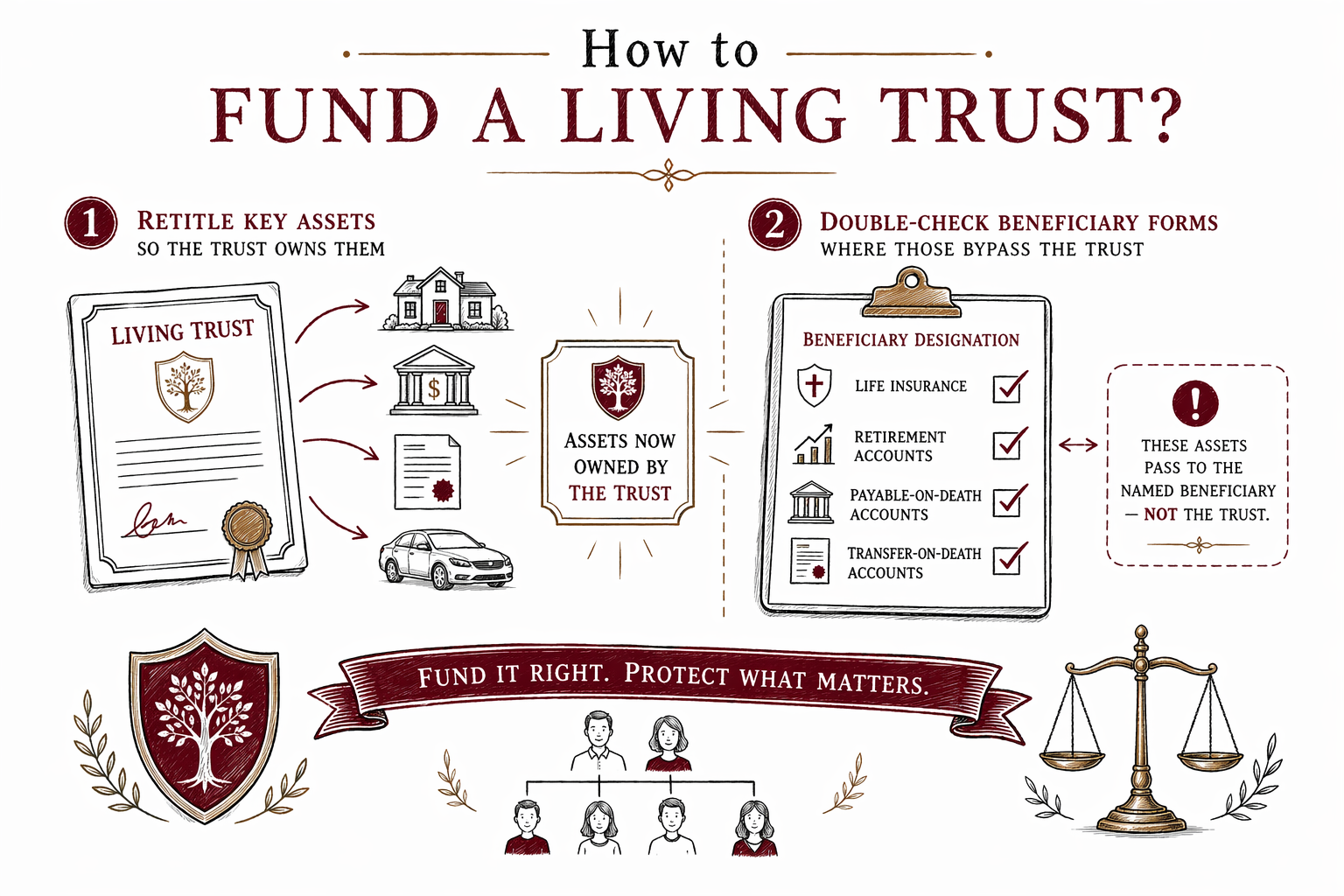

Funding a living trust means retitling or transferring ownership of certain assets so the trust (not just you personally) owns them.

If an asset is titled only in your personal name, it usually won’t be controlled by the trust after you pass—meaning it may still go through probate (rules vary by state).

A properly funded living trust is often the part people miss when planning ahead, especially if they used a template or DIY forms that don’t match their state or their asset types.

A practical checklist: how to fund a living trust (common approaches)

Funding steps are different for each family, but many plans follow a similar order. Your attorney will tailor the list to your accounts, property, and beneficiary forms.

General educational note: this is not legal advice, and probate and trust rules vary by state.

1. Put your trust in place (execute the trust documents) and make sure you have the correct “trust name” used consistently

2. Identify which assets you want the trust to control (often those that would otherwise require probate)

3. Change title where appropriate so the trust is the owner (or the trust is the receiving party), using the exact instructions from your attorney

4. Update account registrations and pay-on-death or beneficiary settings that can bypass a trust

5. Keep records of what you transferred and when, so your family can administer the trust later

What funding often includes: assets commonly moved into a living trust

People most often fund a living trust with “probate-prone” items—things titled in their personal name that would otherwise need court involvement after death.

Common examples include real estate and some bank or brokerage accounts. How you retitle these varies by state and by the account’s rules.

- Real estate deed changes (the trust may become the owner of the property)

- Bank accounts or brokerage accounts retitled to the trust

- Certain business interests or personal property, if you and your attorney decide it fits

What funding often does NOT include: beneficiary designations and “bypass” assets

Some assets are controlled by beneficiary designations or named recipients, not by your trust. Updating those forms is often more important than transferring the asset into the trust.

For example, retirement accounts, life insurance, and some payable-on-death arrangements may pass directly to a beneficiary. That can be good, but it also means a living trust might not control the asset.

Common pitfall: a trust is funded, but beneficiary designations (or titling) are left outdated or inconsistent—so the result doesn’t match what the family intended.

Common pitfalls to avoid (especially with DIY or outdated plans)

Funding is where many living trusts break down, even when the trust documents were signed correctly. Here are frequent issues families run into:

- The trust is never actually funded (a major one): assets stay in personal names

- The trust isn’t titled correctly: the trust’s exact legal name is wrong on deeds or account forms

- An asset is transferred, but the beneficiary forms were not updated where needed

- A “DIY form” doesn’t match your state’s requirements, so it can be harder for the trust to work the way you expected (rules vary by state)

- No clear plan for guardianship or incapacity: a living trust doesn’t automatically replace all other documents people may need

If you’re worried about doing this correctly, a licensed estate planning attorney can walk you through your specific assets and the exact wording your state requires.

How to get help without guesswork: use a free attorney match

If you’re planning ahead and want to make sure a living trust is funded the right way in your state, you can get matched with a licensed estate planning attorney near you.

WillArbor is a FREE matching service (not a law firm and not your lawyer). We collect contact and general planning intent only (such as your state and preferred language)—we do not collect asset values, account numbers, SSNs, or the contents of your documents.

To start: get matched. You can also browse helpful basics at guides and see what attorneys commonly cover under services.

Cost reality check: what funding a living trust usually costs

Estate planning costs vary a lot by state and by what you need—especially the number of assets, whether real estate is involved, and how complex the titling/ownership changes are.

Many attorneys quote estate planning work as a flat fee (not hourly). Typical ranges for a living trust plan can start around a few thousand dollars and go higher for more complex situations, but the real number depends on your documents and your state. These ranges are not quotes.

Because “funding” can involve both document work and account/property retitling steps, ask the attorney what is included in their flat fee and what they charge separately (if anything) for implementation help.

Funding a living trust usually means retitling key assets so the trust, not you personally, owns them—then double-checking beneficiary forms where those bypass the trust.

Common questions

Do I need to fund my living trust right away?

Often, families fund their trust soon after the trust is signed. However, whether you can do it gradually depends on your situation and your state’s rules. An attorney can help you prioritize which assets should move first so your plan works as intended.

If I put my house in the trust, will it avoid probate?

In many cases, transferring a home to a properly funded living trust helps avoid probate for that asset. But probate outcomes can still vary by state and by how the deed and other parts of the plan are handled.

Can I fund a living trust by changing beneficiary designations only?

Sometimes, beneficiary designations control assets and may be the right place to update. But for assets that are titled in your personal name, beneficiary updates alone may not be enough—those assets often need retitling so the trust can own them.

What’s the biggest reason living trusts aren’t effective?

A very common reason is that the trust documents exist, but the trust is never properly funded—assets stay in personal names. Another frequent issue is outdated beneficiary designations or incorrect titling that doesn’t match the trust.

Does funding a trust work the same in every state?

No. Trust and probate laws vary by state, and the titling steps for accounts and real estate can differ. That’s why it’s important to confirm the exact funding steps with a licensed estate planning attorney in your state.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →