Guides

What is a living trust vs. irrevocable trust?

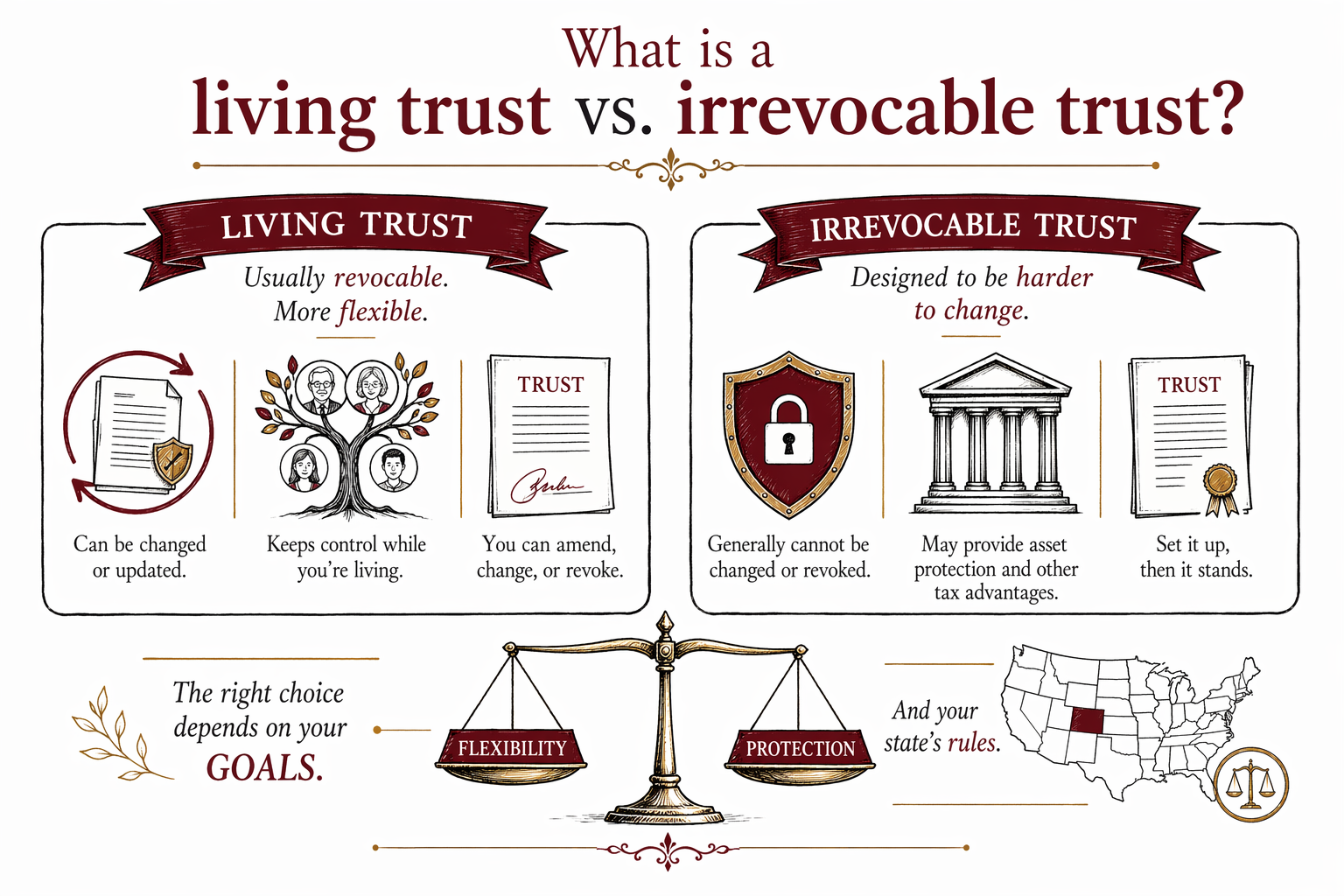

A living trust is usually revocable and helps manage your estate during life and after death. An irrevocable trust is generally harder to change and is used for specific goals, depending on your state.

Quick answer: the main difference

A living trust is typically a “revocable” trust, meaning you can often change it (or cancel it) while you’re alive. People usually choose a living trust to help with organization and to avoid some complications in probate.

An irrevocable trust is usually “irrevocable,” meaning you generally can’t easily change it after it’s created. Because of that, irrevocable trusts are often used when someone wants to permanently set aside property for a particular purpose.

These are general patterns—actual rules depend on state law and the exact wording in the trust document.

What is a living trust (often revocable)?

A living trust is a trust you create during your lifetime. It can hold assets (like property) that you want managed under the trust’s terms.

In many living trust setups, you remain in control while you’re alive: you can typically update the trust, replace who manages it, or cancel it (again, this depends on the state and the document).

After you pass away, the trust usually continues under a plan you set in advance—often directing how and when beneficiaries receive things. Some families also use a living trust to streamline the process after death compared with going through probate for those trust assets.

What is an irrevocable trust?

An irrevocable trust is designed so that, once it’s created, the person who sets it up generally gives up the ability to change it or take the property back.

Why would families do that? Common reasons include putting assets into a structure that can’t be casually altered later, protecting a specific purpose, or creating clearer long-term terms for beneficiaries.

Because it’s hard to modify, an irrevocable trust requires extra care—what you give up and what you keep can be very state- and fact-dependent.

How families decide: what to compare

If you’re choosing between these options, start with your goals—because “living vs. irrevocable” is only part of the picture.

Consider these questions:

1. Do you want flexibility to update plans later?

2. Do you want property to move smoothly after death, without needing probate for trust assets?

3. Are you trying to achieve a specific long-term outcome that benefits from “set it and mostly leave it” terms?

4. Are you comfortable with the limits that come with irrevocable decisions?

A licensed estate planning attorney can explain how your state handles trusts, probate, and trust funding (for example, whether assets must be titled into the trust to get the intended effect). Get matched with a local attorney if you’d like guidance for your situation.

Common pitfalls to watch for

Trusts can help, but they don’t help automatically. Many problems come from misunderstandings or “almost done” documents.

Common pitfalls include:

- Forgetting to fund the trust: a trust usually only controls what is properly transferred or titled into it.

- Relying on DIY forms that don’t match your state: trust requirements vary by state and can be easy to get wrong.

- Out-of-date beneficiary designations: life insurance and retirement accounts often pass by beneficiary forms, not by what’s in a trust (unless coordinated).

- Missing core documents: even with a trust, you may still need powers of attorney and an advance directive for healthcare decisions.

- No clear plan for guardianship of minor children: trusts may not replace a will when it comes to naming guardians.

Also, the idea that a living trust always “avoids probate” is sometimes overstated. The real-world result depends on your state’s probate rules, what assets are in the trust, and how the trust is set up.

Cost, time, and what affects the price (flat fees vary)

Most estate planning work is quoted as a flat fee, not hourly. A typical range for a basic estate plan (often including a will and core documents) may be around a few hundred to a few thousand dollars, depending on the state and complexity.

For trusts, prices can be higher. As a general guide, many families see ranges that can start around the low-to-mid thousands for a relatively straightforward living trust plan and go higher for more complex arrangements. Irrevocable trusts are often more expensive because they require careful drafting and coordination.

What drives the cost up or down:

- Your state (rules and required language vary)

- Complexity (multiple beneficiaries, special conditions, property types)

- Number of documents included (trust + will + powers of attorney + healthcare directive)

- Whether additional planning is needed to coordinate accounts and assets

These are ranges, not quotes. The real number depends on what you need, your state, and the details you discuss with a licensed attorney. A matched attorney should confirm the flat fee in writing before doing any work.

A living trust is usually revocable and more flexible, while an irrevocable trust is designed to be harder to change—so the right choice depends on your goals and your state’s rules.

Common questions

Can I change a living trust after I create it?

Often, yes—many living trusts are revocable, which means you can typically update or cancel them while you’re alive. The exact ability to change it depends on the trust terms and state law.

Is an irrevocable trust ever changed?

Sometimes, but it’s usually limited and not the same as a revocable living trust. Many irrevocable trusts are designed to be “locked in,” and changes may require court approval or may not be allowed at all, depending on the trust language and your state.

Does a living trust replace a will?

Often it can reduce what goes through probate, but it usually doesn’t replace everything a will does—especially guardianship for minor children. Many families use both documents together.

Do I have to put all my assets into the trust?

Only certain assets may be needed, and many states require specific steps to properly transfer or title assets into the trust. An attorney can explain what to fund for the result you want—without relying on guesswork.

Will a living trust automatically avoid probate in every state?

No. Trust and probate rules vary by state and by what property is held in the trust. What you can avoid—and what still might require probate—depends on state law and your setup.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →