Guides

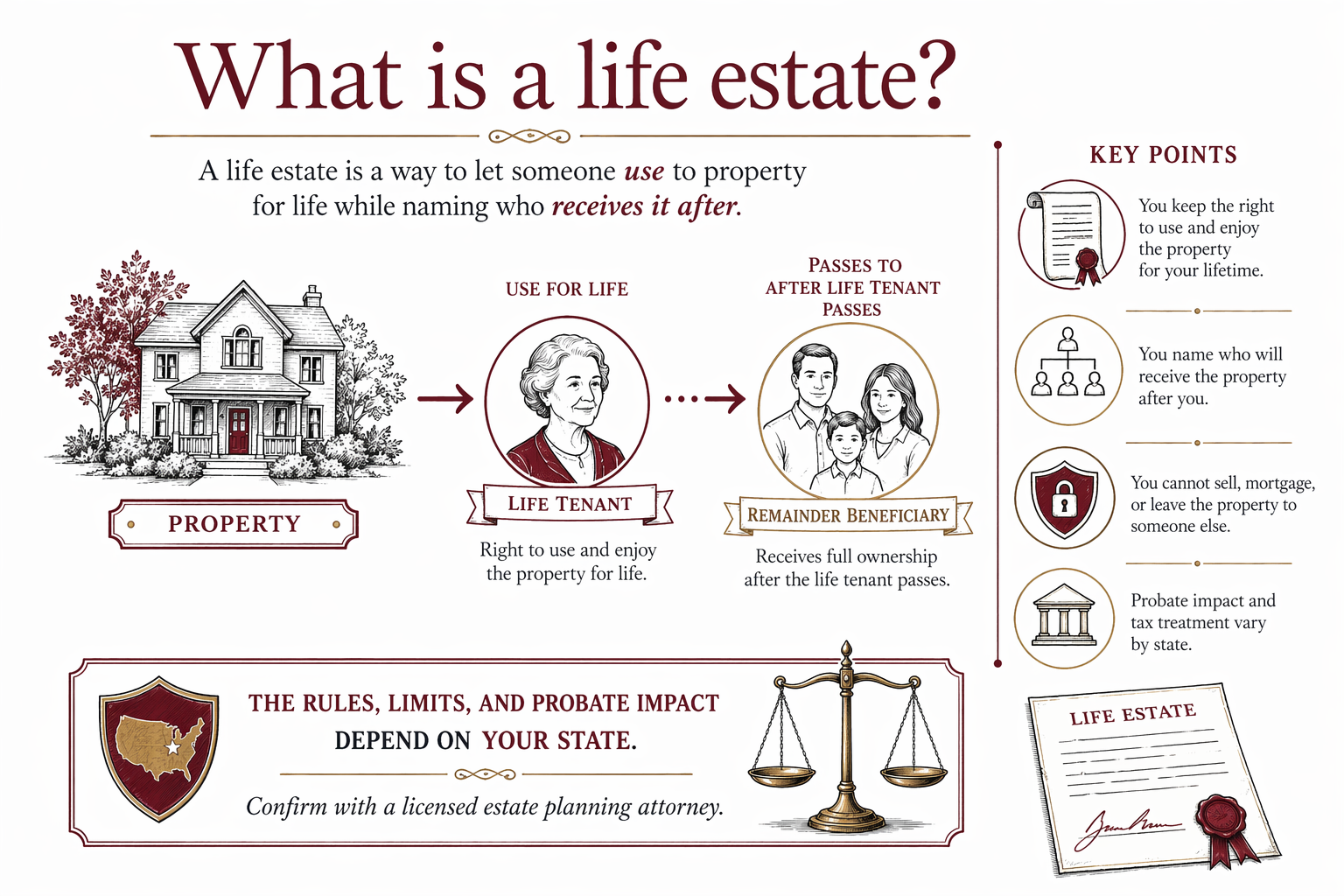

What is a life estate?

A life estate is a property ownership arrangement where someone can use and live in a home for the rest of their life, and another person will own it afterward. It can avoid some probate steps in some situations, but the rules and risks vary by state.

Life estate in plain terms (what it is)

A life estate means “you own it for life,” but with limits.

Usually, one person (the “life tenant”) has the right to live in or use the property during their lifetime. Another person (the “remainder” or “remainder beneficiary”) receives the property when the life tenant’s life estate ends—often at the life tenant’s death.

Whether this avoids probate, how it’s handled, and what paperwork is needed can differ a lot depending on your state.

Two common ways life estates show up in family planning

1) Created during life (often by a deed): A homeowner transfers property to set up the life estate and the remainder beneficiary at the same time.

2) Created by documents (sometimes in estate plans): A life estate can also be discussed as part of a broader plan with a will or trust—though the exact setup matters.

Because the legal details depend on your state, it’s important to talk with a licensed estate planning attorney in your state rather than relying on forms or online instructions.

Why families consider a life estate (and what to know before choosing)

Families often consider a life estate to:

- Keep a home in the family and name who should receive it later

- Reduce uncertainty after a death (for example, by identifying the next owner in advance)

At the same time, life estates can bring trade-offs. In many places, the life tenant may have responsibilities (like maintaining the property and paying certain costs), and they may not be able to freely sell or change the property without consequences for the remainder beneficiary.

Important: life estate rules vary by state, and they can interact with other issues like Medicaid eligibility, property taxes, and creditor claims. Don’t guess—confirm with an attorney licensed in your state.

Common pitfalls to avoid

Life estates can go wrong when the paperwork is unclear, outdated, or doesn’t match how you actually want your family protected.

- Dying without an overall plan: Even with a life estate, a full plan may still be needed for other assets and for guardianship (if you have minor children).

- “DIY” documents that don’t work in your state: Forms found online may not match your state’s laws. A small wording difference can change who gets the property and when.

- Unintended control problems: The life tenant may assume they can sell, refinance, or make major decisions freely, but the remainder beneficiary’s interest can restrict options.

- Out-of-date beneficiary choices: If other related documents (or deed language) don’t reflect your current family situation, disputes can happen.

If you’re unsure what fits your situation, you can start by learning the difference between a will and a trust in our guide: Wills vs. trusts: what’s the difference?.

How to make a decision safely (next steps)

Start with your goal, then match the tool to the goal. For a life estate, key questions usually include:

- Who should get the property after the life tenant’s death?

- What powers and limits will the life tenant have over the property during their lifetime?

- How will this affect probate and other family legal issues in your state?

- Does your broader plan also need a will, power of attorney, or advance directive?

A licensed estate planning attorney can explain the options that fit your state and your family’s priorities. If you’d like, you can get matched for free with an attorney near you through get matched. The family stays in control: compare attorneys, confirm the flat fee in writing before any work starts, and make sure the attorney is licensed in your state.

Cost basics (what life estates often involve)

In most states, setting up a life estate usually involves deed preparation and often coordination with the rest of an estate plan. Estate planning services are commonly quoted as a flat fee (not hourly).

Typical flat-fee ranges you may see for related estate planning work can vary widely, but may fall roughly in the range of $1,000 to $3,500+ depending on the documents needed and the state. This is not a quote—ranges are not guaranteed and the real number depends on complexity.

Prices can go up if you need additional documents (like a will, powers of attorney, or advance directive), if multiple parties are involved, if the property situation is complex, or if your state’s process is more involved. Rules vary by state, so ask for the total flat fee in writing before work begins.

A life estate is a way to let someone use a property for life while naming who receives it after, but the rules, limits, and probate impact depend on your state—so confirm with a licensed estate planning attorney.

Common questions

Does a life estate mean the person owns the house fully?

Not exactly. The life tenant typically has the right to live in or use the property during their lifetime, but ownership interests are split so the remainder beneficiary gets the property after the life tenant’s death. The details and limits vary by state.

Will a life estate avoid probate?

Sometimes it can, but it’s not guaranteed. Whether probate is involved depends on how the life estate is created and how your state handles property transfers. A licensed estate planning attorney in your state can explain what to expect.

Can the life tenant sell or change the property?

Often, there are restrictions because the remainder beneficiary has an interest. Whether and how a sale can happen depends on state law and the exact deed language. Get advice from a licensed attorney before making changes.

Is a life estate the same thing as a living trust?

No. A life estate is usually a deed-based arrangement tied to a person’s life, while a trust is an entity that can hold assets and follow instructions you set. They can both be used in estate planning, but they work differently.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →