Guides

How to leave money to grandchildren?

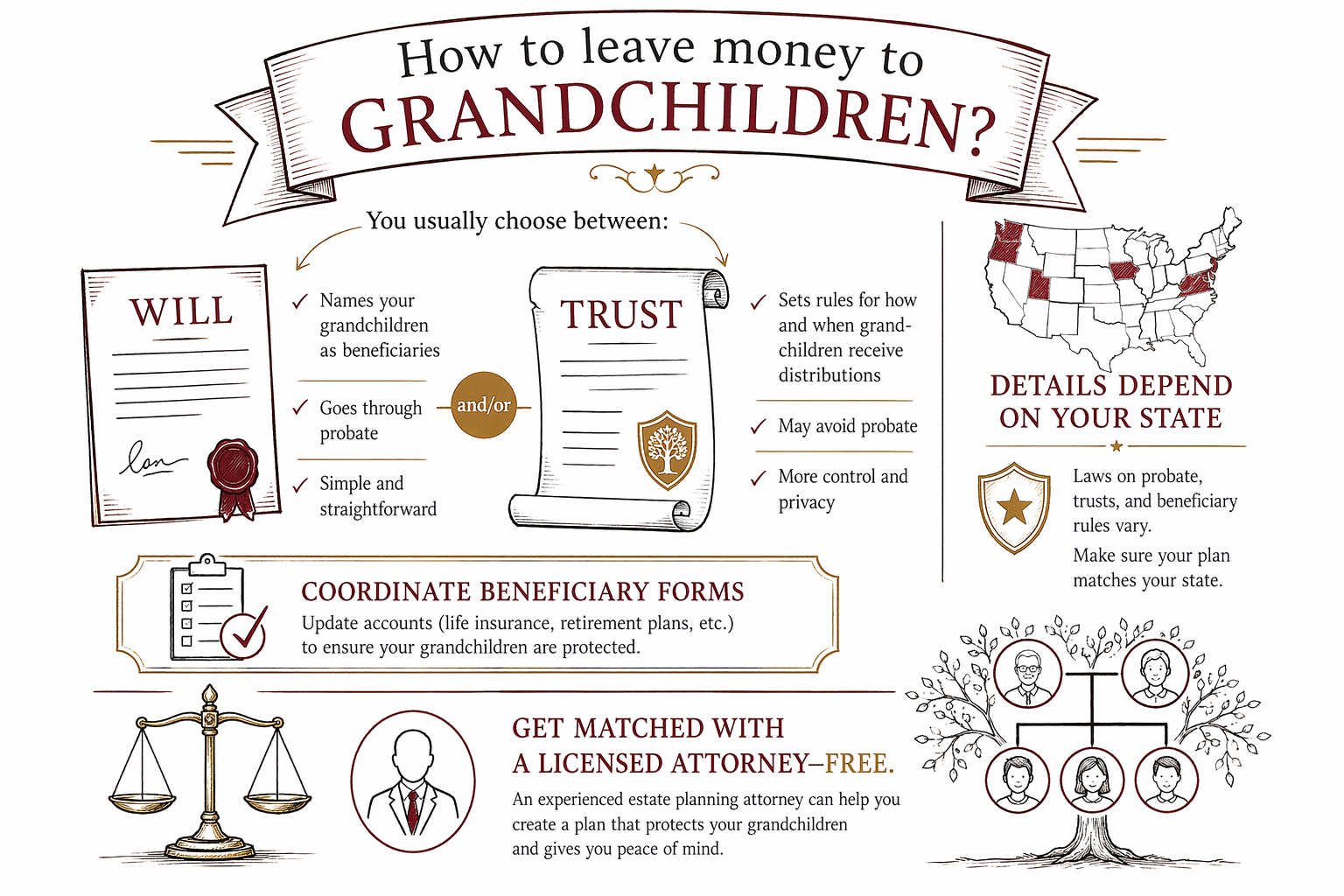

You can leave money to grandchildren through a will, a trust, and—sometimes—beneficiary designations on accounts. The best choice depends on your goals (who controls the money, when they receive it, and whether you want to avoid probate), and rules vary by state.

Answer first: the main ways to leave money to grandchildren

Most families use one (or a mix) of these options: a will, a trust, and beneficiary designations.

A will can name grandchildren as beneficiaries and can also create rules for what happens if a grandchild is a minor or not ready to manage money. A trust can help you control timing and conditions—often starting with a trustee managing funds for a period.

Beneficiary designations apply to certain accounts (like life insurance or retirement accounts) and can pass money to the named people outside of probate, but they must be set up correctly and kept up to date.

Because inheritance and probate rules vary by state—and can be different for minors, trusts, and inherited accounts—this is general education. A licensed estate planning attorney in your state can explain what fits your situation.

Step-by-step: decide what you want for your grandchildren

Start by writing your goal in plain words. This helps you choose the right document and avoids common mistakes.

- Decide “who gets it.” Name the grandchild(ren) and think about what happens if someone dies before you.

- Decide “when they get it.” For example: at age 25, when they graduate, or in stages.

- Decide “who manages it first.” If a grandchild is a minor, a trust with a trustee is often considered; a will can also name a guardian and set instructions.

- Decide whether you want to reduce probate. Some strategies use trusts or beneficiary designations, but the right approach depends on state rules.

If you’re new to the US or not sure what terms mean, that’s okay. A good attorney will explain options in your language or with an interpreter, and you can confirm the plan in writing before anything is drafted.

Will vs. trust (plain explanation) for grandchild inheritances

A will is a legal document that explains who should receive your property after you die. In many families, a will is the simplest way to say “my grandchildren inherit.” It can also name a guardian for minor children and set instructions for how money should be handled.

A trust is a separate legal arrangement where a trustee holds and manages assets for the people you name (beneficiaries). A trust can provide more control—such as managing money for a grandchild until a certain age, or helping avoid some problems that can happen when a minor directly inherits.

Both tools can work. Some families use a will for broad instructions and a trust for specific goals. The best choice varies by state and by your family situation.

Pitfall to watch: a trust only helps if it’s properly funded (assets titled/assigned into the trust as the attorney recommends). An “empty” or unfunded trust may not do what you intended.

Beneficiary designations: useful, but they must match your plan

Many accounts have their own “payable on death” or beneficiary forms. These typically go by the form you completed, not by what your will says.

That means you can accidentally leave money to the wrong person if you never update beneficiaries after life changes (marriage, divorce, deaths, or new grandchildren). Another common issue is having outdated or incomplete beneficiary listings.

Pitfall to watch: out-of-date beneficiary designations can override your will’s instructions. Review your beneficiary forms periodically—especially after major family events.

Also, be careful with DIY changes. State and federal rules about certain accounts and inherited benefits can be complex. A licensed estate planning attorney can help you coordinate beneficiaries with your overall plan.

Common pitfalls families run into when leaving money to grandchildren

Here are the mistakes that come up again and again when families plan ahead:

- Dying without a will (“intestacy”): state law decides who inherits, and it may not include your grandchildren the way you would choose.

- No named guardian (if relevant): if you have children, your grandchildren are connected to that decision too.

- DIY forms that fail in your state: documents created for one state may not work in another.

- Out-of-date beneficiary designations: your will can’t always override beneficiary forms.

- An unfunded trust: you intended control, but assets weren’t moved into the trust.

- Leaving control unclear: if you don’t specify timing or management, your intent can be harder to follow.

If any of these sound familiar, you’re not alone. The good news is that most problems can be corrected by reviewing and updating your plan with an attorney.

Rules vary by state, so it’s important to get advice in your state—not just general information.

How much does estate planning typically cost? (Honest ranges)

Cost varies a lot by state, by how many documents you need, and by how complex the plan is (for example: multiple grandchildren, minors, a trust, or special conditions). Most estate planning is quoted as a flat fee—not an hourly rate.

As broad, educational ranges you may see in the US (not a quote):

- Basic will: often around $500 to $1,500

- Will + powers of attorney + advance directives: often around $800 to $2,500

- Living trust plan (trust + pour-over will) with common add-ons: often around $2,000 to $4,500

- More complex plans (for example: multiple trusts, complex family situations): can be higher

These are ranges, not promises. Your real price depends on your documents and your state. A licensed attorney should explain what’s included and confirm the flat fee in writing before doing any work.

WillArbor is a free matching service—not a law firm. You’ll decide whether to hire an attorney, and participating attorneys pay a flat fee to be part of the service (the service is free for families).

Get matched to a licensed estate planning attorney (free for families)

If you want to leave money to your grandchildren, the next step is to talk with a licensed estate planning attorney in your state. They can explain options for your situation and the rules that apply where you live.

WillArbor helps you get connected with an attorney near you. The service is FREE for the family, and we only collect basic contact information plus what you want to plan and your preferred language.

Use these next steps:

1. Explore our guides to learn the basics first.

2. Review what estate planning services can include (wills, trusts, powers of attorney, and advance directives).

3. Then get matched with a licensed estate planning attorney in your state.

Remember: WillArbor is not your lawyer and does not draft documents. Confirm the attorney is licensed in your state and that the flat fee (not an hourly charge) is agreed to in writing before work begins.

To leave money to grandchildren, you usually choose between a will and/or trust (and coordinate beneficiary forms), but the details depend on your state, so get matched with a licensed attorney—free through WillArbor.

Common questions

Can I leave money to grandchildren in my will even if they are minors?

Often, yes. A will can name grandchildren as beneficiaries, but if they are minors, the plan usually needs clear instructions about who manages the money and when the minor can receive it. This is state-specific, so an attorney in your state can explain the safest, most practical approach.

Will a trust automatically handle everything for my grandchildren?

Not automatically. A trust usually must be properly funded (assets assigned to the trust as your attorney recommends). If the trust isn’t funded, your intended benefit may not happen.

If my will says one thing, but my account beneficiary forms say another, what happens?

In many cases, beneficiary forms can control for certain accounts, even if your will says something different. That’s why reviewing and updating beneficiary designations is a common and important part of estate planning.

How do I avoid probate when leaving money to grandchildren?

Some strategies can help reduce probate, such as using certain trusts and beneficiary designations. Whether it works the way you expect depends on your state’s probate rules and how your assets are titled—so it’s best to review the plan with a licensed attorney.

What documents do I usually need to leave money to grandchildren?

Many families need at least a will, and sometimes a trust, plus related planning documents such as powers of attorney and advance directives. The right set depends on your goals and your state’s rules.

Related help

The difference between a will and a living trust, when each makes sense, and why many families use both.

Open → How to Avoid ProbatePlain-language ways families reduce or avoid probate — trusts, beneficiary designations, and joint ownership.

Open → What Happens If You Die Without a WillIntestacy explained: how your state decides who inherits when there is no will — and why that may not match your wishes.

Open →